Bike insurance or two wheeler insurance covers damages to your vehicle from natural calamities or man-made disasters. With the ongoing monsoon season, having a two wheeler insurance policy becomes essential due to an increasing number of potholes on the road and higher probability of floods in most parts of India. Natural catastrophe like floods, earthquakes, cyclones and storms can damage your two wheeler thereby leading to huge loss of expense. Hence, it is wise to have a bike insurance policy for your two wheeler. Furthermore, unforeseen scenarios like burglary, fire, theft, vandalism, road accidents, etc., can cause significant damage to your vehicle. With two wheeler insurance policy, you can ride with peace of mind as the insurer will bear the complete cost of repair expenses due to these aforementioned events. Also, riding 2 wheeler insurance policy without third party two wheeler insurance policy is a punishable offence as per the Motor Vehicles Act of 1988. Therefore, buy or renew bike insurance online if it's nearing expiry. A two wheeler insurance policy will cover your vehicle against own damages and third party liabilities. It is indeed necessary to have a bike insurance policy. You can choose from comprehensive bike insurance, third party bike insurance cover and standalone own-damage cover. However, it is advisable to completely safeguard your vehicle by buying comprehensive two wheeler insurance. You can customize the comprehensive bike insurance policy by adding unique add-ons like no claim bonus protection, emergency roadside assistance, zero depreciation, etc to enhance your two-wheeler insurance policy. HDFC ERGO offers two wheeler insurance for all types of two-wheelers, such as motorcycles, moped bikes/scooters, electric bikes/ scooters, and more and has a wide network of 2000+ cashless garagesˇ

| Key Features | Benefits of HDFC Ergo Two Wheeler Insurance |

| Claim settlement | AI-enabled tool IDEAS |

| Own Damage Cover | Covers accident & natural or man-made calamities |

| Third Party Damage Cover | Covers third party injuries and property damages |

| Choice of Unique Add-ons | Customise bike insurance policy with by selecting choice of add-ons like zero depreciation, emergency roadside assistance, etc. |

| Claim Settlement Ratio | 100% Claim Settlement Ratio^ |

| Bike Insurance Premium | Starts at ₹538* |

| Personal Accident Cover | Up to ₹15 lakhs~* |

| Cashless Garage Network | 2000+ ˇ all across India |

| Policy Buy Time | Less than 3 mins |

| Repair Service | Door Step Two Wheeler Repairs° |

| Emergency Roadside Assistance°° | With emergency roadside assistance you can get your bike repaired anywhere and anytime. |

| No Claim Bonus | Up to 50% |

| IDV Customization | Yes |

| Buying & Renewal Process | Online |

| Liability Cover | Yes |

| Add-on Covers | 8 Add-on Covers |

HDFC Ergo offers 4 types of two wheeler insurance like Comprehensive insurance,Third Party insurance, and Standalone own damage car, and cover for a brand new bike. You can further enhance the protection of your bike by adding add-on covers to your comprehensive bike insurance.

COMPREHENSIVE TWO WHEELER INSURANCE Third Party Cover Standalone Own Damage Cover Cover for Brand New Bikes COMPREHENSIVE TWO WHEELER INSURANCEYour two wheeler will be protected against theft, fire, natural or artificial disasters, and more with a comprehensive bike insurance policy. Additionally, you can use the cashless repair option at network garages in India.

It is required to have at least a third party liability two wheeler insurance policy in India, as per the law (Indian Motor Vehicles Act, 1988). However, getting a comprehensive bike insurance policy is advised.

Suitable for bike lovers seeking all-rounded protection, this plan covers:Third party bike insurance covers you for all third party liabilities (property damage, bodily injuries, and death) in any accident involving the insured' s two wheeler.

The cap for compensation for third party property damage is ₹ 1 lakh. However, a court of law determines the amount of compensation in cases of third party bodily injury/death.

Suitable for those who use the bike infrequently, this plan covers:A standalone own damage bike insurance covers any damage you cause to your two wheeler by accident. It provides financial coverage against damage to your bike and not the third party involved in the collision. In addition, own Damage bike insurance policy reimburses you for the costs associated with repairing or replacing any parts of your two wheeler damaged in an accident.

Suitable for those who already have a valid third party cover, this plan covers:Cover for a brand new bike under two wheeler insurance policy offers one year coverage against damage to your own bike along with a five year cover against damages to a third-party person/property.

Suitable for bike lovers seeking all-rounded protection, this plan covers:Been in an accident? Keep calm, we cover damages your bike sustains in an accident.

We won’t let a fire or an explosion burn your finances to ashes, be rest assured your bike is covered.

Your bike getting stolen could be your worst nightmare come true, but we ensure your peace of mind is not disrupted.

Calamities can wreak havoc and your bike is not immune to them, but your finances are!

Your safety is our priority, in case of injuries due to a two wheeler accident we cover your treatment charges.

Damaged a third party property or person? We cover damages to a third party property or injuries sustained by a third party person.

General wear and tear of spare parts or depreciation in the value of your bike or scooter is not covered under bike insurance policy.

Electrical or mechanical breakdown like engine getting seized due to driver’s negligence is not covered under bike insurance policy.

The policyholder cannot claim under a bike insurance policy if the insured vehicle meets with an accident where the rider was driving without a valid driving license or under the influence of alcohol.

This add on cover is available with comprehensive bike insurance cover and it does not consider depreciation rates at the time of claim settlement. With zero depreciation add-on cover, the policyholder will get the entire claim amount for damaged part without any deduction of depreciation value.

With no claim bonus protection add on cover, the NCB benefit is retained despite making claim in a policy year. With this add-on cover, you can raise two claims in a policy year without losing the accumulated NCB.

With Emergency Assistance add on cover you can get support from us any time 24*7, if your two wheeler breakdown in the middle of a highway.

Return to invoice add on cover will help you get claim amount equivalent to your two wheeler's invoice value when you bought it, if the bike or scooter is stolen or it is beyond repair.

Engine and gear box protectors add on cover will cover repair and replacement cost of engine and gearbox child parts. The coverage is offered if damage is due to water ingression, leakage of lubricating oil and damage to gear box.

This add on cover under the two wheeler insurance policy covers consumables items like engine oil, lubricants, brake oil, etc.

With this add-on cover, the insurer will pay you cash allowance of Rs 200 per day if your insured vehicle is in the garage for repair of the damage done due to an insurable peril. The cash allowance will be paid for maximum period of 10 days in case of repair for partial loss only.

With EMI protector add on cover, the insurer will pay equated monthly installment amount (EMI) to insured as mentioned in the policy if the insured vehicle is kept in garage for accidental repairs for more than 30 days.

The more comprehensive is the coverage, the more claim is that you can get. To this end, HDFC ERGO offers a selective range of add-ons with its comprehensive bike insurance policy. Have a look

This add on cover is available with comprehensive bike insurance cover and it does not consider depreciation rates at the time of claim settlement. With zero depreciation add-on cover, the policyholder will get the entire claim amount for damaged part without any deduction of depreciation value.

No claim bonus (NCB) ProtectionWith no claim bonus protection add on cover, the NCB benefit is retained despite making claim in a policy year. With this add-on cover, you can raise two claims in a policy year without losing the accumulated NCB.

Emergency Assistance CoverWith Emergency Assistance add on cover you can get support from us any time 24*7, if your two wheeler breakdown in the middle of a highway.

Return to InvoiceReturn to invoice add on cover will help you get claim amount equivalent to your two wheeler's invoice value when you bought it, if the bike or scooter is stolen or it is beyond repair.

Engine & Gear Box ProtectorEngine and gear box protectors add on cover will cover repair and replacement cost of engine and gearbox child parts. The coverage is offered if damage is due to water ingression, leakage of lubricating oil and damage to gear box.

HDFC ERGO has great news for Electric Vehicle (EV) owners! We're introducing new add-on covers tailored specifically for EVs. These add-ons include protection for your battery charger and accessories, coverage for your electric motor, and a unique zero depreciation claim for the battery charger. By adding these covers, you can shield your EV from potential battery damage caused by unexpected events like floods or fires. As the heart of your EV, safeguarding your batteries and electric motor is a smart move. These three add-ons can be seamlessly added to your comprehensive or standalone own damage cover. The battery charger accessories add-on offers protection against damage due to fires and natural disasters like earthquakes or floods. The electric motor cover ensures coverage for any damage to your EV's motor and its components. And with the zero depreciation claim for the battery charger, you'll be compensated for any depreciation when replacing the battery, including the detachable battery, charger, and accessories. Don't miss the chance to secure your electric vehicle – opt for these add-on covers and drive with peace of mind.

Purchasing insurance for bike is essential for maintaining legal compliance and establishing a financial safety net.

The Motor Vehicles Act, 1988, states that bike insurance is compulsory for all bike owners. If you fail to comply with this requirement, it will be considered a violation of the law, and you must pay fines and penalties.

If you get insurance, you can be confident of having financial security and mental tranquillity because you are acting responsibly and morally. When you purchase and renew two-wheeler insurance on time, you protect yourself and your two-wheeler from unanticipated occurrences.

According to the law, you must pay for the loss a third party incurred if you caused the accident. Having insurance for bike will help you cover any expenses resulting from property damage, accidents, or fatalities. Consequently, you can give the victims prompt compensation.

In case you meet with an accident, you do not have to worry about unexpected additional expenditures. The insurance for bike will cover the repair costs to get your two-wheeler back in form.

Purchasing comprehensive bike insurance can make you feel secure, knowing that it protects you from the possibility of bike theft or loss due to fire. The key is setting the IDV in a range close to the bike's estimated current market worth.

A general misconception amongst bike owners is that you cannot file a claim if a natural calamity damages your bike. However, that is not the case. When a natural or man-made disaster such as floods, tsunamis, or quakes damages the bike, your insurance policy for bike comes to your aid.

Before you buy two wheeler insurance online, you should consider following factors:

Check whether insurer have a huge network of cashless garages. A large number of network garages will not only give multiple location options but also ensure quick claim settlement. HDFC ERGO has a wide network of 2000+ cashless network garages.

Choose an insurer with a high claim settlement ratio, as your claim settlement will be done easily with such insurance providers. HDFC ERGO has a record of 100% claim settlement ratio.

The premium for a two-wheeler insurance policy will depend on various factors like the age of the vehicle, type of policy, and geographical zone.

IDV is the current market value of the vehicle. IDV is the maximum amount that can be claimed on insurance in case of total loss or theft. Generally speaking, IDV decreases as the age of the bike increases.

Riders are add-ons that can be added to comprehensive bike insurance policies by paying an extra premium. You can choose add-on covers like zero depreciation, emergency roadside assistance, engine gearbox protection, etc. It is advisable to avoid choosing add-on covers which are unnecessary or does not have any meaning to you. By choosing unwanted add-on covers, you will end up paying higher two wheeler insurance premium.

Buying bike insurance online from HDFC ERGO gives you the option to avail different plan and discounts by which you can save on premium.

With HDFC ERGO insurance policy for bike you get doorstep repair service from our wide network of cashless garages.

HDFC ERGO bike insurance policy offers AI tool IDEAS (Intelligent Damage detection Estimation and Assessment Solution) for claim settlements. The IDEAS supports instant damage detection and calculation of the claims estimate for the surveyors to help in motor claims settlement in real-time.

With HDFC ERGO bike insurance policy you can opt for emergency roadside assistance add-on cover where vehicle can be repaired anytime and anywhere.

With an annual premium starting at just ₹538, you should look to buy or renew bike insurance online from HDFC ERGO.

With HDFC ERGO Two Wheeler insurance you can insure following type of two-wheelers:

With our two wheeler insurance policy you can safeguard your expense from bike damage due to unforeseen events like floods, earthquakes, fire, theft, riots, terrorism, etc. Bike comes with manual gear transmission, hence it is wise to choose own damage insurance or comprehensive insurance plan, where you can opt for add-on like engine and gearbox protector. Also, comprehensive insurance policy will provide complete coverage for your bike.

Scooter are gearless two-wheeler, with our two wheeler insurance policy you can insure this type of vehicle. You will get coverage for losses due to man-made disasters and natural calamities.

With our two wheeler insurance policy you can also insure your electric bike (Ebike). If you purchase bike insurance for your electric vehicle two-wheeler, it is wise to buy add on covers like protection for your battery charger and coverage for your electric motor.

It is advisable to insure mopeds, which are small motorcycles generally having cubic engine capacity less than 75cc. By insuring moped with HDFC ERGO two wheeler insurance policy the policyholder will get covered for accidental damages, man-made disasters and natural calamities.

Here are useful tips to help you choose the right bike insurance policy as per your requirements and budget: -

1. Know your Coverage :Requirement Before looking for bike insurance plan, it is essential to make an assessment based on your requirement and budget. While buying bike insurance policy you can choose between third party cover and comprehensive cover. Depending upon the usage of your two wheeler, you should choose bike insurance plan that offers coverage as per your requirement.

2. Understand Insurance Declared Value (IDV) : IDV is the current market value of your bike. IDV is the maximum sum insured fixed when purchasing a bike insurance policy and is the amount that insurer will pay in case of total loss or theft of two wheeler. Therefore, IDV is one of the most critical factors determining the two wheeler insurance premium.

3. Look for Add-on to Extend your Bike Insurance Cover : Look for riders that you can add to your bike insurance policy. This will make the coverage more exhaustive. You will have to pay an additional premium for bike insurance for the riders.

4. Compare Bike Insurance Online : It is wise to compare bike insurance online and check the available plans to make an informed decision. You can compare bike insurance plans online based on the coverage offered.

The bike insurance premium rate for comprehensive cover depends on certain external factors such as engine capacity, vehicle age, location, etc. The engine cubic capacity of the bike plays a significant role in determining bike insurance premium rates. On the other hand, IRDAI determines the price of the third-party policy, which also affects the price of a comprehensive bike insurance policy. The table below explains the third-party bike insurance premium rates in India with effect from 1st June, 2022.

| Engine Capacity (in CC) | Annual third party bike insurance rates | 5-years third party bike insurance rates |

| Up to 75 cc | Rs 538 | Rs 2901 |

| 75-150 cc | Rs 714 | Rs 3851 |

| 150-350 cc | Rs 1366 | Rs 7,365 |

| Above 350 cc | Rs 2804 | Rs 15,117 |

The Insurance Regulatory and Department Authority of India (IRDAI) considers the electric bike motor’s kilowatt capacity (kW) for calculating the premium for third party insurance of E-bike. Here are the third party electric bike insurance premiums.

| Electric Two-wheelers with kilowatt capacity (kW) | Premium rate for 1-year policy | Premium rate for long-term policy (5-year) |

| Not Exceeding 3 kW | INR 457 | INR 2,466 |

| More than 3 kW but not exceeding 7 kW | INR 607 | INR 3,273 |

| More than 7 kW but less than 16 kW | INR 1,161 | INR 6,260 |

| Exceeding 16 kW | INR 2,383 | INR 12,849 |

Before buying a bike insurance policy, you should be thoroughly aware about its coverage. Apart from this, you should also know the inclusion and exclusion of the plan you are buying. Here are some ways by which you can compare two wheeler insurance plans:

1. Premium Break-up: Always ask for a premium break-up of your two wheeler insurance policy. A clear break-up will help you get clear idea for what you are paying for.

2. Own Damage Premium: Own damage bike insurance provides coverage if your bike is stolen or faces any other kind of damage due to an insurable peril. When you are checking the premium of own-damage, here are some of the things that you need to know about:

• IDV: IDV or Insured Declared Value refers to the market value of your bike. The IDV is directly proportional to the bike insurance premium, hence lower the IDV, lower will be the bike insurance premium.

• NCB: NCB or No Claim Bonus in bike insurance is the benefit given to the policyholder if they do not raise any claim in a given year. If a person has an accumulated NCB, then their bike insurance premium will be lower. However, it is important to renew your bike insurance plan within 90 days after its expiry to take advantage of NCB benefits

3. Third-party Bike Insurance Premium: Third party bike insurance provides coverage for third party liabilities. Typically, third-party bike insurance provides a financial coverage of up to Rs. 1 lakh for any damage to third party property or person. In addition, there's unlimited coverage for the death or disability of another person involved in an accident by the insured person's vehicle. This amount is decided by court.

4. Personal Accident Premium: In bike insurance, it is mandatory to have a Personal Accident Cover. This type of cover is only meant for the policyholder. So, even if you own multiple vehicles, you will still need a single Personal Accident cover.

5. Add on premium - Choose your add-on cover wisely. Buying add on cover which are not required for your two wheeler will unnecessarily increase the premium.

Every insurance company offers two types of insurance policy for two wheelers. The third party cover is the bare minimum policy which is mandatory by the Indian law and covers only third party damage. The comprehensive cover policy provides all round protection and provides coverage against theft, natural and man-made mishaps, and accidents along with third party damage.Considering the benefits it offers, the premium for a comprehensive cover will be more as compared to the premium for third party cover.

Different bikes have different specifications and therefore, the cost of insuring them is also different. A bike engine’s cubic capacity is the deciding component that affects the insurance premium. Higher the cubic capacity, higher will be the insurance premium. In addition, the age of the vehicle, type of bike model and class of the vehicle, place of registration, fuel type, and the number of miles covered also affect the premium price.

Not many people are aware but your age, gender, driving record and driving experience can also affect the insurance premium. In such instances, companies calculate the associated risk factor and accordingly charge the premium. For example, a young driver (in the early 20s) with a year of driving experience will be charged a higher premium as compared to a middle-aged, experienced bike driver.

The current price or market value of the bike also affect the insurance premium. The market value of the bike depends upon its brand and functionality. If the vehicle is old, the premium is decided based on the condition of the vehicle as well as its resale value.

Add-on covers can help in increasing the coverage, but the more the number of add-ons, the higher will be the premium. Therefore, choose only those covers that you deem necessary.

Many people love adding accessories to their bikes in order to improve its aesthetics and performance. However, these modifications are usually not covered under the standard insurance policy and you might need to purchase an add-on cover for these modifications. However, adding these modifications under your insurance policy can increase the premium amount.

In recent years the purchase of two wheeler insurance policy has shown a tremendous increase. This is due to the latest law by the government, where a person driving without a bike insurance policy can lead to heavy penalties or imprisonment. Third Party insurance premium is fixed by IRDAI which depends on CC of your bike. The premium of other insurance policy for bike depends from company to company, and the amount depends on various factors such as registration date, location, IDV etc. However, if you are still looking to save your two wheeler insurance premium, here’s how it can be done.

1.Maintain a clean driving record: Ensure that you ride safely and avoid meeting with an accident. By this you will avoid raising any claim, which can help you avail no claim bonus benefit during bike insurance renewal.

2. Opt for higher deductibles: If you pay higher amount while raising claim, you can save on premium during renewal of bike insurance.

3. Avail Add-ons: You can customise your comprehensive bike insurance policy by selecting add-ons like zero depreciation cover, no claim bonus protection, emergency roadside assistance, etc.

4. Security Device installation: Install devices like anti-theft alarm which can help reduce bike insurance premium.

5. Compare two wheeler insurance online Also Read : 5 Ways to Save On Bike Insurance

One of the vital factors that help you decide the type of bike insurance policy to choose is the premium you need to shell out for it.You can look at how you can calculate your premium with a bike insurance premium calculator. A premium calculator is a simple tool that helps you to determine the exact premium you will have to pay to buy the two wheeler policy of your choice. Here is how you can calculate your bike insurance premium with a two wheeler insurance calculator:

1. Enter your vehicle’s details, like registration year, registration city, make, model, etc.

2. Select comprehensive bike insurance policy or third party bike insurance policy.

3. Select a choice of add-on like zero depreciation, no claim bonus protection, emergency roadside assistance, etc., if you opt for a comprehensive bike insurance policy.

4. Click on bike insurance price.

5. The bike insurance premium calculator will show the exact two wheeler insurance premium and help you buy the policy that fits your budget perfectly.

You can pay through a secured payment gateway and get the insurance policy for the bike instantly via WhatsApp or your registered email address.

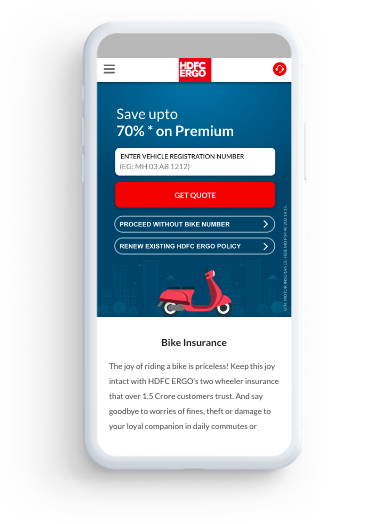

Enter your registration number

Select your policy cover*

(Incase we are not able to auto fetch your vehicle details, we will need just a few details of your vehicle

- Make, model, variant, registration year and registration city)

Provide your previous policy

and No Claim Bonus (NCB) status

Get your bike insurance quote instantly!

There are numerous benefits of buying bike insurance online from HDFC ERGO website. Let us take a look at few benefits of buying comprehensive insurance policy online:

Get instant quotes - With the help of bike insurance calculators, you get instant premium quotes of your bike insurance policy. Enter your bike’s details, and the premium will be displayed, inclusive and exclusive of taxes. You can also opt for add-ons with your comprehensive insurance policy and get the updated premium instantly.

Quick issuance - You can get a bike insurance policy within few minutes if you buy online. You have to fill an online application form, provide the bike details, pay the premium online, and the policy is sent to your email id.

Minimal paperwork - Buying bike insurance online only requires a few documents. You have to upload your bike’s registration forms, details, and KYC documents when you buy the policy for the first time. After that, you can opt for bike insurance renewal or port your plan without any paperwork.

Payment reminders - After you buy a bike insurance policy online, you get regular bike insurance renewal reminders from our end to renew your coverage continuously. This ensures that you enjoy uninterrupted coverage.

Seamlessness and transparency - HDFC ERGO’s bike insurance policy buying process is seamless and transparent. You need to follow some simple steps to buy bike insurance online, and there are no hidden charges. What you see is what you pay

Buying or renewing your bike insurance policy is always advisable if your two-wheeler is in good condition and actively used on the road. You can also change your insurance company while renewing your bike insurance policy. There are two ways you can buy or renew bike insurance online.

Step 1. Click on the bike insurance product on HDFC ERGO website and fill in the details, including your bike registration number and then click on get quote.

Step 2: Choose between comprehensive and third party liability cover.You can also edit your Insured declared value if you opt for comprehensive plan. You can choose plan from one year to three years.

Step 3: You can also add personal accident cover for passenger and paid driver. Furthermore, you can customise the policy by choosing add-on like emergency roadside assistance cover, zero depreciation, etc

Step 4: Give details about your last bike insurance policy. E.g. Previous policy type(comprehensive or third party, policy expiry date, details of your claims made, if any)

Step 5: You can now view your bike insurance premium

Pay the premium via a secured payment gateway.

The two wheeler insurance policy will be sent to your registered email address or via WhatsApp.

If HDFC ERGO policy has expired, you can visit bike insurance renewal section. However, if expired policy doesn’t belong to HDFC ERGO, please visit bike insurance page

Step1: Visit the bike insurance section on HDFC ERGO website and select renew the policy.

Step 2: Enter details associated with your HDFC ERGO policy that you want to renew, include or exclude add-on covers, and complete the journey by paying the bike insurance premium online.

Step 3: The renewed bike insurance policy will be mailed to your registered email-id or your WhatsApp.

Two wheelers are a prevalent mode of transportation in India as its pocket friendly and easy to commute. For those who can't afford a new bike, a second-hand bike is a good option. Secondhand bike insurance is an essential part of buying a used bike or a scooter. Unfortunately, many fail to insure their bike or transfer bike insurance. Like regular motor insurance, second-hand two-wheeler insurance protects you from damage and losses caused to a third party or yourself while riding your pre-owned bike. Before buying second-hand bike insurance, remember the following things:

• Ensure the new RC is in the new owner's name

• Check the Insured Declared Value (IDV)

• If you have an existing bike insurance policy, get the No Claim Bonus (NCB) transferred to get a discount

• Choose from several add-on covers (emergency roadside assistance, no claim bonus protection, zero depreciation cover,etc)

We offer you a comprehensive policy that meets all your concerns. In addition, the insurance plan covers for various benefits to keep your finances safe against unforeseen events relating to your two wheeler.

Step 1. Visit the HDFC ERGO website's bike insurance section, enter your secondhand bike registration number, and click on get a quote.

Step 2: Enter your secondhand bike make and model.

Step 3: Give details about your last secondhand bike insurance policy.

Step 4: Select between a third party bike insurance and a comprehensive bike insurance plan.

Step 5: You can now view your bike insurance premium.

Step1: Click on the bike insurance product on the HDFC ERGO website and select renew the policy.

Step 2: Enter details of your secondhand bike, include or exclude add-on covers, and complete the journey by paying the bike insurance premium online.

Step 3: The renewed bike insurance policy will be mailed to your registered email-id.

Even if your bike is old, you have to buy/renew two wheeler insurance. Not only it is mandatory as per the Motor Vehicles Act of 1988 but it also protects loss of expense from vehicle damage due to an unforeseen events. Let us see how to buy/renew two wheeler insurance for an old bike

Step 1: Click on the bike insurance icon on HDFC ERGO website home page. Fill in the details, including your bike registration number and then click on get quote.

Step 2: Choose from comprehensive, standalone own damage and third party liability cover.

Step 3: You can also add personal accident cover for passenger and paid driver. Furthermore, if you choose comprehensive or own damage cover you can customise the policy by choosing add-on like emergency roadside assistance cover, zero depreciation, etc

Step 4: You can now view your bike insurance premium

Pay the premium via a secured payment gateway.

The two wheeler insurance policy will be sent to your registered email address or via WhatsApp.

Here’s why you should renew two wheeler insurance online via HDFC ERGO:

With our bike insurance premium calculator, you can check your premium instantly. Just enter your two-wheeler’s registration number, choose policy, select appropriate add-on if required, the premium would be displayed, both inclusive and exclusive of taxes.

If you buy or renew bike insurance online via HDFC ERGO website, the policy will be mailed to you instantly on your registered email ID.

After you buy two wheeler insurance online you get a regular reminder to renew your policy from our end. This ensures that you enjoy uninterrupted coverage and do not violate traffic rules by having a valid third party two wheeler insurance policy.

Buying bike insurance online will save you from the hassle of paperwork. You can buy two wheeler insurance from HDFC ERGO website within few minutes just by entering few details and the soft copy of your policy will be mailed on your registered email ID or on your WhatsApp number.

If you buy bike insurance online you pay what you see on your mobile or desktop screen. There are no hidden charges. Also, you avoid paying any money to middlemen.

Here’s why you should renew expired two wheeler insurance

Uninterrupted Coverage – If you renew expired two wheeler insurance on time, your vehicle will remain covered from losses arising due to unforeseen events like flood, theft, fire, etc.

Avoid Losing No Claim Bonus (NCB) Benefit – By doing timely renewal of your bike insurance policy you can keep your NCB discount intact and avail that when you renew two wheeler insurance. If you do not renew the policy within 90 days of its expiry date, your NCB discount will lapse and you will not be able to use its benefit during policy renewal.

Adherance to the Law – If you ride your bike with expired two wheeler insurance policy, traffic cop can penalize you for Rs 2000. As per the Motor Vehicles Act of 1988 it is mandatory for two wheeler owners to have at least the third party cover of bike insurance policy.

Whenever you are planning to buy or renew two wheeler insurance online, it is always best to have a duplicate two wheeler insurance copy in hand. Here’s how you can get a duplicate two-wheeler insurance copy online

• Step 1: Visit our website.

• Step 2: Then click on the help button icon on the homepage. Then click on email/download policy copy.

• Step 3: Enter your policy details like policy number, mobile number, etc.

• Step 4: Then, enter OTP as prompted. Also, verify your profile if asked.

• Step 5: After verification, view, print, or download your two-wheeler policy.

If you are planning to buy a two wheeler insurance, you should first understand the difference between long term and annual bike insurance plan. The comparison shown in the table below will help you make an informed decision.

| Features | 1 Year Policy | Long Term Policy |

| Policy Renewal Date | Annual bike insurance policy has to be renewed every year. | For long term two wheeler insurance policy you will have to pay the premium just once in three or five years, thereby saving you from policy lapses. |

| Flexibility | With short term bike insurance policy you can modify your plan. | After purchasing long term insurance policy, you cannot modify it for three years or five years. |

| Cost-Effectiveness | One year insurance policy is prone to price hikes on a yearly basis | A long-term bike insurance policy is cost-effective as it avoids any increase in the annual premium which could be imposed by the IRDAI. |

| Add-ons | You can add or remove add-on covers every year in 1 year bike insurance policy. | In long term policy, you can buy add-on covers only at the time of purchasing the policy |

| No claim bonus discount | Here NCB discount is less in comparison to long term policy. | Here NCB discount is at a higher rate compared to long term policy. |

Insurance providers offer incentives to the policyholder for responsible driving called a No Claim Bonus (NCB). The bonus is a reduction in the bike insurance policy premium cost. The insured person can avail NCB benefits if he/she does not raise any claim during the previous policy year. The NCB discount goes upto 50% if you do not raise any claim for five consecutive years.

The most significant advantage is that NCB enables you to obtain the same level of coverage for a significantly lesser price. However, NCB discount lapse if you do not renew policy within 90 days of its expiry date.

NCB Slab for Bike

| Claim free year | NCB Discount (%) |

| After the 1st Year | 20% |

| After the 2nd Year | 25% |

| After the 3rd Year | 35% |

| After the 4th Year | 45% |

| After the 5th Year | 50% |

Example: Mr.A is renewing his two wheeler insurance policy. This will be the second year of his policy and he has not raised any claim. He can now avail 20% discount on two wheeler insurance renewal. However, if he renews his policy after 90 days of its expiry date, he won’t be able to use his NCB benefits.

IDV , or insured declared value in an insurance policy for bike, is the maximum sum for which your motorcycle may be covered by insurance. This is the insurance payout if the two-wheeler is lost or stolen without a trace. In other words, the Insured Declared Value of your bike is its current market value.

While the actual IDV of the bike is calculated using the formula published by the IRDAI, you would have the option to change the value by a 15% margin.

You would get a larger sum as compensation in the event of a total loss or theft if the insurer and the insured mutually agreed upon the higher IDV. Nevertheless, it would be best if you didn't arbitrarily raise the IDV because you would be paying a higher premium for nothing more.

On the other hand, you shouldn't reduce the IDV just to reduce the premiums. For starters, you would not receive adequate compensation for theft or total loss and would have to pay more out of pocket to obtain a replacement. Additionally, all claims will be honoured in proportion to the IDV.

Calculation of IDV

The IDV of bike insurance is calculated based on its listed selling price at the time when the vehicle was first purchased and the time elapsed since then. The amount to be depreciated is determined is fixed by the IRDAI. The current schedule of depreciation is provided below:

| Age of the Vehicle | % of Depreciation for fixing IDV |

| Less than 6 months | 5% |

| Exceeding 6 months but less than 1 year | 15% |

| More than 1 year but not exceeding 2 years | 20% |

| Exceeding 2 years but less than 3 years | 30% |

| More than 3 years but less than 4 years | 40% |

| More than 3 years but not exceeding 4 years | 50% |

Example – Mr. A has fixed Rs 80,000 IDV for his scooter, the insurer will pay larger sum of compensation to Mr.A if his bike suffer damages due to theft, fire or any unforeseen events as he has kept his IDV accurate as per the market selling price. However, Mr.A will have to pay higher premium. However, if Mr.A reduces his scooter’s IDV amount, he will not get large compensation from insurer during claim settlement but his premium will be low in this scenario.

If you wish to opt for add on covers along with comprehensive two wheeler insurance policy, you should understand differences between popular riders like zero depreciation and return to invoice (RTI).

| Factor | Zero Depreciation | Return to Invoice (RTI) |

| Definition | Zero depreciation cover enables easier claim settlement without considering the bike’s depreciation value. | RTI cover provides the insured with a lump-sum claim amount based on IDV in case the bike is stolen or damaged beyond repair. |

| Coverage Duration | Zero depreciation usually covers for up to 5 years. | Return to invoice extends cover for 3 years or less. |

| Who is it For? | Usually beneficial for bikes less than 5 years old. | Usually beneficial for new bikes or bikes below the age of 3. |

| How Does it Work? | Zero depreciation covers the gap between depreciated value and the cost of repairs. | It helps fill the gap between the IDV and the invoice value of the two-wheeler during claim settlement. |

As your bike ages, its depreciation increases, so the IDV goes down. So, for older bikes, the IDV is lower than newer ones.

Your bike's make, model and variant (MMV) determines its market value. Different bikes are priced differently, and when you buy 2-wheeler insurance, the make and model of the bike are required to determine the IDV. Based on the MMV, the bike's market value is determined, and then the applicable depreciation is deducted to arrive at the IDV.

If you add accessories to your bike, which are not factory fitted, the value of such accessories will be part of your IDV calculation. In such cases, IDV would be calculated using the following formula – IDV = (market value of the bike – age-based depreciation of the bike) + (market value of the accessories – depreciation on such accessories)

As your bike ages, its depreciation increases and, so, the IDV goes down. Therefore, if the registration date of your bike is older, then the IDV will be less than the newer ones.

Your bike's make, model and variant (MMV) decide its market value. Different bikes have different prices, so when you buy two wheeler insurance, the make and model of the bike are required to determine the IDV. Based on the MMV, the bike's market value is determined, and after deducting the applicable depreciation, we get the IDV.

Depreciation is the decrease in the value of your bike brought on by normal wear and tear over time.

One of the most popular 2 wheeler insurance add -on covers is zero depreciation two wheeler insurance, sometimes called "nil depreciation." With comprehensive bike insurance or a standalone own damage two wheeler insurance policy, Zero Depreciation add -on coverage is available.

All your bike’s parts are insured at 100%, except the tyres, tubes, and batteries, which are covered at 50% depreciation.

You must add a zero depreciation add-on cover to your basic bike insurance plan to receive the total bike insurance claim settlement amount without suffering any reductions.

Who should opt for the Zero Depreciation add-on coverage?

• New motorists

• New owners of two wheelers

• People who reside in accident-prone regions

• People who own expensively equipped luxury two wheelers

Filing a claim for bike insurance policy just got easier with our 4 step process and a claims settlement record that will ease your claim related worries!

Get in touch with our claim team by calling on our helpline number or sending a message on WhatsApp on 8169500500. With the link provided by our agent, you can upload documents online.

You can opt for self inspection or an app enabled digital inspection by a surveyor or workshop partner.

Track of your claim status through the claim tracker.When your claim is approved you will get the notification through the message and it will be settled through network garage.

You need to go through following steps for cashless claim in bike insurance

• File an FIR at the nearest police station in case of property damage, bodily injury, theft and major damages.

• Locate network garages on our website.

• Drive or have your vehicle towed to the nearest network garage.

• All damages / losses will be surveyed and assessed by our surveyor.

• Fill in the claim form and provide the related documents as mentioned in the form.

• You will be updated through SMS/Emails on every stage of the claim.

• Once the vehicle is ready, pay your share of the claim consisting of Compulsory deductible, depreciation etc to the garage and drive off. The balance would be settled by us directly with the network garage

• Receive the claims computation sheet with entire break up for your ready records.

Here are list of documents required to make claim for two wheeler insurance under following conditions:

• Proof of Two wheeler Insurance

• Copy of Bike’s RC, and original tax receipts for verification

• Police FIR report while reporting a third party death, damage and bodily injuries

• Copy of your original driving license

• Damage repair estimate.

• Payment receipts and repair bills

• Original Two wheeler Insurance Policy Documents

• Theft endorsement from the concerned Regional Transport Office

• Original RC Tax payment receipt

• Service booklets/bike keys and the warranty card

• Previous Two Wheeler Insurance Details like two wheeler insurance policy number, insurance company details and duration of the policy period

• Police FIR/ JMFC report/ Final investigation report

• An approved copy of the letter addressing the concerned RTO regarding the theft and declaring the bike as "NON-USE."

• Original Bike Insurance Policy Documents

• Soft copy of the Registration Certificate of the bike

• Soft copy of the Driving License of the rider

• Present evidence of the incident through photographs or videos

• FIR (if required)

• Report of the fire brigade (if any)

| Brochure | Claim Forms | Policy Wordings |

| Get details about the insurance policy's key features, coverages and deductibles in the brochure. Two wheeler insurance brochure will help you know in-depth about our policy. . | Smoothen up your claim process by getting the two wheeler insurance claim form. | It is important to know about situations and conditions under which you can get loss coverage under the two wheeler insurance policy. Please refer to the two wheeler insurance policy wordings to know the terms and conditions. |

I recommend getting your two wheeler insured from HDFC ERGO, a brand serving more than 1.6 Crore+ Happy Customer@. With vast number of cashless network garages and quick customer service, you can be assured of help in event of any damage to your vehicle. Also one should insure his/her vehicle and avoid getting heavily fined under the recently enacted Motor Vehicle Amendment Act 2019.

Our customers have rated us View all 1,54,266 Reviews

Your customer care executive provided continuous support after I raised my concern and diligently followed up to get it to a closure. I appreciate the customer care team's efforts. Thanks.

I felt happy after talking to your officials, wherein I got the correct policy. Overall my buying experience was awesome.

I have been using the HDFC ERGO policy for 4 years. Whenever I raise any doubts to the customer care team, I get a good response.

I would like to appreciate your customer care executive effort for giving quick solution and support. I want HDFC ERGO to continue giving best services to their customers.

My query was resolved on the same day. The policy can be easily downloaded from HDFC Ergo website. I am overall happy with the customer service of your team and would love to continue with HDFC Ergo.

I have been renewing my insurance with HDFC ERGO for the past two years. Everything is good. I would rate the HDFC ERGO policy 9/10.

I am very satisfied with your customer service. I had contacted your team for claim intimation and the turnaround time for settling claim was short.

Your customer care team understood my concern and gave me the appropriate solution quickly. Special thanks to your back office team who promptly replied to my queries and got it resolved.

I recently registered the claim at HDFC ERGO. The turnaround time for the claim settlement was just 3-4 working days. I am happy with the prices and the premium rates that HDFC ERGO offers. I appreciate your team's support and assistance.

HDFC ERGO provides fantastic customer service, and all the executives are outstanding. It is a request that the HDFC ERGO continue to provide the same service and immediately clear their customer doubts like they have been doing for many years.

HDFC ERGO provides excellent services. I would choose this insurer for buying more insurance policies. I would like to thank the HDFC ERGO team for good services. I recommend my relatives and friends to choose HDFC ERGO for buying bike insurance and other insurance policies.

I appreciate the speedy and efficient service provided by your customer care team. In addition, your customer executives are well trained as they answered all my queries and had the intent to help the customer. They patiently listen to the customer's query and solve it perfectly.

I wanted to correct my policy details and to my surprise the HDFC ERGO team was so quick and helpful unlike my experience with other insurers and aggregators. My details were corrected the same day and I want to express my gratitude to the customer care team. I promise to remain a HDFC ERGO customer always.

I wanted to correct my policy details and to my surprise the HDFC ERGO team was so quick and helpful unlike my experience with other insurers and aggregators. My details were corrected the same day and I want to express my gratitude to the customer care team. I promise to remain a HDFC ERGO customer always.

2 Min Read

Union Minister Nitin Gadkari on 4th September, 2024 urged two-wheeler companies to provide helmets to buyers at a discounted price. He emphasized the fact that many road accident fatalities occur due to the lack of helmet use. The road transport and highway minister also spoke about his ambition to start driving school in every taluka of the country.

Published on September 5, 2024

2 Min Read

Ola electric two-wheeler has stepped into the electric bike segment and has now launched its first electric bike in the Indian market. The Ola Roadster electric bike launched on 17th August 2024 has a long range of 579km. However, only the Pro variant will have a range of 579km, while the standard model will have a range of 248km.

Published on August 20, 2024

2 Min Read

Retail sales of electric two-wheelers saw a smart month-on-month rise in July 2024 to 106,949 units. The sales volume has increased by 34% on June’s 79,868 units and 96% year-on-year. This strong growth was expected as the now-extended electric-mobility promotion scheme 2024 (EMPS) was to have ended on July 31 with e-scooter and bike buyers advancing their purchase decisions ahead of that date.

Published on August 5, 2024

2 Min Read

The two-wheeler segment roars in the rural market in the first half of 2024. According to the Federation of Automobile Dealers Associations, rural contribution to two-wheeler sales increased by 57-60% in the first quarter of 2024-25. In the rural market, there is a continued popularity of motorcycles over scooters because the former are ideal for rural roads and conditions.

Published on July 25, 2024

2 Min Read

Two-wheeler brands like Honda, Hero MotoCorp and TVS have witnessed good sales in June 2024. However, brands like Royal Enfield did not enjoy good sales in June 2024. Hero MotoCorp sold over 5.03 lakh units last month. While Honda’s two-wheeler sales surpassed 5.18 lakh units. Royal Enfield has witnessed a year-on-year decline in its sales while Suzuki and Bajaj two-wheelers have had a y-o-y growth in June 2024.

Published on July 03, 2024

2 Min Read

A man while filling his bike's petrol tank in Maharashtra is seen taking his phone out of his pocket to attend a call when suddenly, a fire erupts. Electromagnetic waves from mobile phones can reportedly induce current and generate an electric spark in nearby metal conductors, thereby causing a fire. In this case, the fire is also believed to have been triggered by a spark from the phone, which is why phones are prohibited at petrol pumps.

Published on June 14, 2024

On purchase of comprehensive policy, you can get a personal accident cover as an add-on, which will help you or your family financially in case of the accidental death or injuries. You can also purchase this cover for a pillion driver. Getting a personal accident cover is mandatory and one can now purchase the same as a standalone policy. Read this blog on benefits of personal accident insurance policy.

As per the Motor Vehicles Act of 1988, it is compulsory to ride a two-wheeler with a valid third party cover. If you ride your bike/scooter without it, you could be fined by RTO for ₹ 2,000 or imprisonment of up to three months. If it is a 2nd-time offence, you are liable to pay a fine of ₹ 4,000 and/or imprisonment of up to three months.

As per the Motor Vehicles Act, a person can only be legally allowed to drive a vehicle if the latter has been duly insured by an IRDA approved insurance provider. A thirds party insurance is a must for every vehicle and if the driver is found to be operating the vehicle without a valid insurance, they will be issued a challan of Rs 2000. This is for the first offence! If you are caught riding a bike without valid insurance a subsequent time, your challan will be doubled to Rs 4000. The court can also sentence you to three months jail time or community service.

Online Bike Insurance Policy renewal is a prompt way of ensuring that your bike enjoys continued insurance coverage. The procedure to renew your bike insurance online is

• Log onto the website of the bike insurer

• Go to the login portal and enter your login id and password

• Click on the renewal button and enter details of your two wheeler insurance policy if needed

• Choose any Add-On covers that you need and click on the submit button

• Pay the renewal premium using debit card, credit card or online banking

• Save the online receipt carefully and also get a hard copy of the same

The policy gets lapsed if it is not renewed before the due date. However, the expired policy can be renewed in two ways – online and offline. To renew it online, log on to the official website of the insurance company and enter the policy details. After this, you will be asked to make payment. Once the payment is done, your policy will be renewed and policy documents will be sent to your registered e-mail within a few minutes. If you wish to do it offline, you have to take your bike to the nearest branch for inspection along with the necessary documents. No inspection is required if you opt for online renewal. Read here the reasons to renew your bike insurance immediately.

Renewing two wheeler insurance online is very simple. Visit the website of the insurance company, enter details such as bike model, purchase date of bike etc. and choose any add-ons. Once you make the payment, your policy will be renewed.

It is wise to buy bike insurance online as it is easy and hassle free. There is no risk of any fraudulent. Furthermore, there is no paperwork involved as everything is digital and the policy is mailed to you on your registered email ID. In addition to these benefits, you also compare different policies easily online and check out for different discounts.

Bike insurance renewal must be done before the expiry of your existing policy so you can enjoy uninterrupted coverage. Insurance providers usually send reminders to their customers before policy expiration. But by chance, if you miss the deadline, you can renew it even after expiry. However, if you delay it more than 90 days, you will lose your No Claim Bonus and will have to pay more insurance premiums. Also, a delayed renewal would mean a fresh inspection of the vehicle, which may reduce its Insured Declared Value (IDV).

Both options are available. As a customer, you should pick a policy that gives you maximum benefits at a lower premium. However, when you decide to continue with the same insurance provider, you get more loyalty benefits like a decrease in deductibles or an accident forgiveness option.

When buying car insurance online, the common documents required are proof of identity (any one of these - driver’s license, passport, Aadhar, PAN card, government issued ID card), proof of address (any one - driver’s license, passport, bank or post office passbook, government issued address proof), recent passport size photograph, driver’s license,and registration certificate of the car.

As per the Supreme Court’s recent mandate, a personal accident (PA) cover is compulsory for the owner/driver of two wheelers. The policy can be bought as a standalone cover or along with your two wheeler insurance, and provides compensation to the owner in case of death, bodily injuries or any permanent disability due to an accident. It is not mandatory for the pillion rider.

As per the Indian Motor Vehicles Act, 1988, it is compulsory for two wheeler riders to have a valid Third-Party insurance policy. This insurance, also known as Liability Only Insurance Policy or Act Only Policy, protects riders against any damages caused to a third party (person or property) in case of an accident caused by the insured two wheeler, given the accident was not deliberate or wasn’t done under the influence of any drugs or alcohol. A Comprehensive Insurance Policy provides additional coverage for damage or theft of the two wheeler along with the benefits mentioned in the Third Party insurance policy. It safeguards the vehicle against losses/damages caused by natural calamities like flood, lightning, earthquakes, etc. or malicious acts like theft, riots, strikes, and terrorist activity, among others.

This differs from one insurance company to another but there are some events which will not be covered by any company. These include any damage done to the vehicle due to drunken driving or in case the driver does not have a valid driving license, wear and tear, ageing of the vehicle, damages to tires and tubes unless damaged due to an accident, mechanical or electrical breakdown and failure, theft of accessories unless the bike is also stolen. If your bike suffers losses outside the country, this will also not be covered.

The value of your vehicle depreciates or reduces with the passage of time. While settling a claim, the insurer deducts this depreciation value and you have to pay a larger part of the claim amount. But, if you have zero depreciation cover, the insurance company will pay the entire claim amount without deducting the depreciation amount. You need to pay an additional premium to purchase zero depreciation add-on. Read this blog to know more on zero depreciation cover in Two Wheeler insurance .

Add-on cover is the additional cover that you can buy to boost the coverage of your insurance policy. The add-on covers are not included in the comprehensive two wheeler insurance and need to be purchased with an additional premium. Some add-ons that you can opt for are zero depreciation cover, return to invoice, engine and gear protection, emergency assistance cover and no claim bonus protection.

If you fail to renew the insurance policy of your two wheeler within 90 days of the expiration, you will lose your No Claim Bonus (NCB). Therefore, make sure you always renew the policy within the time frame.

In case of damages to your two wheeler or theft, you should first lodge an FIR. After that you should file a claim, and the documents required for the same are RC book, active DL, policy document, FIR copy, duly signed claim form, photos taken at the accident spot and any other document as needed by the insurer.

Yes, you can do that. By not making a claim if the damage is minimal, you would get an extra discount on the premium the following year. For example, in your first year, if you get a 20% discount, then by not making any claims the whole year, you would get an additional 5%-10% discount the following year.

Yes, there is. Usually, insurance companies prefer that policyholders make a claim within 24 hours of the accident or theft, failing which the claim might get rejected. However, some insurers might consider if there is a genuine reason for delay in filing the claim.

No. If the policy is not renewed on or before the expiry date, it becomes inactive, and you will not be covered during the grace period.

No. Your insurance company is not liable to pay for any claims, even if it expired just a day before the accident.

The surveyor will make an inspection to check the extent of damage done to your two wheeler before you send it to a garage. The surveyor will make an estimate of the repair cost and submit the report to the insurance company for further processing.

In case of a cashless claim, you just have to pay for the deductibles and the rest of the bill will be taken care of by your insurance company. However, you can only use cashless claim services in your insurance company’s network garages. The reimbursement claim gives you the flexibility to choose any garage of your choice, but you have to pay the full amount of the bill and get it reimbursed later.

Some common reasons for claim rejections are policy lapse, providing incomplete or false information, loss that is not covered in the policy, filing the claim after deadline, driving without valid DL, driving in an intoxicated state, and false claims. Read this blog to know more reasons for claim rejection.

There will be no change in the bike’s insurance policy, but the premium will change depending on the place to which you will move. Metro cities usually have a higher premium than the rest of the country. Whether it is a location or job change, you have to inform the insurance company so that your details can be updated.

The Insured Declared Value (IDV) is the current market value of your vehicle. It is calculated by subtracting the depreciation cost of the vehicle from the manufacturer’s selling price. The registration cost, insurance cost and road tax are not included in the IDV. And, if accessories are fitted later, IDV of those are calculated separately.

You should contact your insurance provider and request them to include the required changes in your two wheeler insurance policy.

While selling your bike, it’s important to transfer your insurance policy to the bike’s new owner. By doing so, you will be free from all liabilities if the bike is involved in any accident in future. However, the No Claim Bonus, accumulated in your policy, can be transferred to your name which can be used for your new vehicle. You also have the option to cancel the existing policy at the time of selling.

Yes, you can transfer the current insurance to your new vehicle. You have to inform the insurance company about the change in vehicle and also pay the difference in premium, if any.

Yes, you are eligible for discount on your insurance premium if you install anti-theft devices certified by the Automotive Research Association of India (ARAI). This is because an anti-theft gadget reduces the risk factor for the insurer.

Visit the official website of the insurance provider or Regional Transport Office or the State Transport Department. You can also visit the official website of the Ministry of Road Transport and Highways – VAHAN (https://parivahan.gov.in/parivahan/). Enter your bike’s registration details to know the policy number and insurance status.

When a policyholder files a cashless claim, the insurance company pays for all the repair work but the repairs should be done in any of the insurance provider’s network garages. The bill is sent directly to the insurance company and after verification of all the details, the payment is made. In reimbursement claim, the policyholder pays for the repairs and the amount is reimbursed by the insurer after verifying the original bills, receipts, etc. In this type of claim, you can get your bike repaired at your preferred garage and get it reimbursed.

In case of theft or ‘total damage’, the owner will be paid the insured declared value of the bike. The insurance company may hire a private investigator to track the stolen bike. In such cases, the claim settlement process can take a little longer. To ensure there are no anomalies, the policyholder should immediately file an FIR, intimate the insurer and RTO, and keep the required documents ready.

Yes, the policy can be cancelled anytime during the policy period. But to get the refund, there are some terms and conditions of the insurance company which you must comply with.

To get a duplicate copy of the policy online, log in to your account by visiting the official website of the insurance provider, enter details such as policy number, name etc. Once you get the document, download and print it. In the offline process, you have to inform the insurer, file an FIR at the nearest police station, and write an application providing details like policy number, name etc. and how the document was lost. Lastly, you need to sign a bond with the insurer for a duplicate copy of your policy document.

The premium amount depends on factors such as the type of insurance taken, claims history, model of the bike, age and the registration location of your bike. Click here to read more.

Riding a two wheeler with an expired insurance policy is a punishable offence. You can renew it within 90 days to retain certain benefits such as No Claim Bonus. After the said period, the policy can’t be renewed and you will have to buy a new policy through proper documentation and verification procedure.

A comprehensive plan provides protection against damage to your own vehicle and as well as that of the third party. Apart from accidents, it also covers theft and damage to the vehicle by any natural calamity like floods, storms etc. and man-made reasons like riots and vandalism. Buying the third-party policy is mandatory according to the law while experts recommend bike owners to opt for a comprehensive policy for bigger coverage.

Zero Depreciation Cover is an add-on cover to your existing policy. The value of the bike reduces over the years. The reduced market value is due to the depreciation rate. The moment a brand new vehicle leaves the showroom, it loses 5-10% of its value as its next buyer would be buying a second-hand vehicle. So, even if you have opted for the comprehensive insurance policy, the claim money you will get after the theft or total loss of the bike will be according to the depreciated value of the bike parts. For example, if the depreciated value of your Rs. 90,000 bike is Rs. 60,000, you will get the latter. However, if you have Zero Depreciation Cover, you will get Rs. 90,000. This add-on cover eliminates the depreciation factor.

Once you opt for Emergency Assistance Cover, you get round-the-clock assistance to mitigate any technical or mechanical breakdown issues. This add-on benefit covers minor repairs on-site, punctured tyres, battery jump starts, refuelling the tank, lost key assistance, duplicate key issue, and even towing charges up to 100 km from your registered address. In some cases, the insurer also bears the expenses related to accommodation if the policyholder needs a place to stay while the bike is being repaired.

According to the Ministry of Road Transport and Highways, digital copy of documents such as driving license and a vehicle’s registration, insurance etc., which are stored in Digilocker or mParivahan mobile app, are accepted legally. Original papers or photocopies of the same are no longer mandatory. The printout of the softcopy of your two wheeler insurance policy serves as the original document.

Yes. Most insurance companies in India offer discounts on the premium if the policyholder is a member of Automotive Research Association of India (ARAI).

Electrical and non-electrical accessories are fittings which people make in their vehicles. Electrical accessories usually include music system, fog lights, LCD TV, etc. The non-electrical accessories are seat covers, wheel caps, CNG kit and other interior fittings. Their value is calculated according to their initial market value and then the depreciation rate is applied.

Add-ons are not included in the comprehensive insurance. To enhance the coverage, you have to buy the add-on covers by paying a little extra premium. Some add-on covers are zero depreciation cover, road assistance, engine protection, return to invoice.

To buy bike insurance online, the documents required are proof of identity (driving license/passport/Aadhar card/PAN card/government issued ID card), proof of address (driving license/passport/bank or post office passbook/government issued address proof), recent passport size photograph, valid driving license, registration certificate of the bike, net banking/credit card/debit card details (for online payment).

Inspection of a vehicle is mandatory if you renew your vehicle offline after the expiry date. You have to take your bike to the insurer for inspection along with the necessary documents.

The best policy is the one that gives you maximum benefits at a lower premium. You can compare offers to see which plan suits your needs the best. However, buying an insurance policy online is faster and hassle-free as you don’t need to visit the insurer’s office or get a policy from a certified insurance agent. The online process will help you get some discounts as the insurance company can save on agent commissions and pass on that benefit to you.

The main difference between the two lies in the coverage. Third-party insurance covers only the damages caused to the third party due to an accident, while comprehensive insurance provides complete protection against damage to your own vehicle as well as that of the third party involved in an accident. Comprehensive insurance also protects your two wheeler against theft, accidents, and damage due to natural calamities such as floods, cyclone, etc. Third-party insurance is mandatory as per the Motor Vehicles Act, 1988. Read here for further information.

If someone borrows your bike and causes damages to the bike or a third-party then your bike insurance will still cover for the losses and damages as mentioned in the policy wording. However, you need to have proper documents of the bike and the policy. Also, you won’t be compensated if the rider was riding in a drunk state or without a valid two wheeler licence.

The insurance will not be of any use in this case. If you meet with an accident while riding someone else’s bike, you will not be eligible for any claim as you are not a registered user of the bike.

Visit the official website of your insurer and then login to your account to check the policy details. If you face issues while logging in, refer to the policy document sent to your registered email id.

Insurance premium is the amount of money which the insured pays periodically to the insurer to keep the policy active. The cost of premium depends on factors like age of the insured, location, type of coverage, and claims history. Failure to pay the premium on time can lead to lapse of the policy.

Over the years, the documentation process has become quite simplified. When buying a policy online, you may need to provide some basic information like identity proof, address proof, driving license information, registration number and registration certificate (RC) number of your vehicle and a few passport-sized photographs.

Any change or modification in the existing insurance policy is done through an endorsement. In other words, an endorsement is a document in which modifications in the policy are incorporated. The modifications are not made in the original copy but in the Endorsement certificate. Endorsements are of 2 types - premium-bearing endorsement and non-premium bearing endorsement.

The Insured Declared Value (IDV) of your bike is the sum insured coverage you can claim in case of total loss or damage to your two wheeler. Simply put, it is the current market value of your two wheeler. The bigger the IDV, the higher will be the insurance premium.

– IDV is nothing but the market value of your vehicle. It is only valid under comprehensive bike insurance policy. Insured Declared Value is what your bike is valued in the market after calculating the depreciation on it. For example, you buy a brand new bike of Rs 80,000 (ex-showroom price). Your IDV at the time of purchase will be Rs 80,000, but as your bike gets older, its value starts to depreciate and so does the Insured Declared Value.

You can calculate your bike’s IDV by subtracting the depreciation on vehicle’s part from its current market value. The registration cost, road tax and insurance cost are not included in the IDV. Also, if there are accessories that have been fit later, IDV of those parts will be calculated separately.

| Age of the Bike | Depreciation % |

| 6 months and below | 5% |

| 6 months to 1 year | 15% |

| 1-2 years | 20% |

| 2-3 years | 30% |

| 3-4 years | 40% |

| 4-5 years | 50% |

| 5+ years | IDV mutually decided by the insurer and policyholder |

So if you are planning to renew two wheeler insurance, it is advisable to declare the correct IDV to your insurer because your claim amount depend on this. Unfortunately, if your vehicle is stolen or totally damaged during an accident, your insurer will refund the entire amount to you, mentioned on your insurance policy IDV.

Depreciation means a reduction in the value of your vehicle and its parts over the years of usage. When making a claim, you may end up paying a large amount from your pocket since the insurance company deducts the depreciation amount charged against the damaged parts. But opting for a zero depreciation cover as an add-on under comprehensive insurance for a bike can help you save on out-of-pocket expenses. This is because the insurance company would bear this cover's depreciation amount charged against the damaged parts.

NCB is a discount on the premium given to the insurer for having a claim-free policy term. A no claims bonus ranges from a discount of 20-50% and is something an insurer can earn at the end of your policy period by not making a single claim during the previous policy year.

You can’t get a no-claims bonus when you buy your first comprehensive bike insurance policy; you can only get it on bike insurance renewal. If you buy a new bike, you will be issued a new bike insurance policy, but you can still avail of the NCB you accumulated on the old bike or policy. However, suppose you do not renew your scooter insurance or bike insurance policy within 90 days from the actual date of the policy expiration. In that case, you cannot avail benefits of NCB.

Your NCB comes in only after the first renewal of your comprehensive two wheeler insurance policy. Do note that NCB exclusively applies to the damage component of your premium, which is the premium calculated based on IDV of the bike minus the bike’s wear and tear cost. The bonus does not apply to third party cover premium. You begin with receiving a 20% discount on your premium after the first claim-free year. The discount increases by 5-10% at the time of policy renewal each year (as shown in table below). After five years, the discount will not increase, even if you don’t raise a claim in a year.

| Claim Free Years | No Claim Bonus |

| After 1 year | 20% |

| After 2 years | 25% |

| After 3 years | 35% |

| After 4 years | 45% |

| After 5 years | 50% |

You can avail of this cover under the comprehensive bike insurance policy. With this add-on cover, HDFC ERGO offers you round-the-clock assistance to deal with emergency breakdown issues. The emergency assistance cover includes minor on-site repairs, lost key assistance, duplicate key issues, tyre changes, battery jump starts, fuel tank emptying and towing charges. For instance, if you face an accident and damage your bike/scooter, it must be towed to a garage. With this add-on cover, you may call the insurer, and they will get your vehicle towed to the nearest possible garage up to 100 km from your declared registered address.

A driving license (DL) is the legal document which authorizes an individual to ride vehicle on road. In order to ride or drive a vehicle legally on the public roads, an Indian driving licence is mandatory. A learner's license is issued for learning. A month after the learner's licence is issued, the person has to appear for the test in front of an RTO authority, who upon proper examination, will declare if he/she has passed the exam or not. On passing the examination, a person can get a permanent driving license. Also, as per the Motor Vehicle Act, a person driving a vehicle without a licence cannot claim the insurance. If you caused an accident and were not carrying a DL, you are not eligible for third party claims. Any such insurance claims will be rejected by the insurance company and you are liable to pay the amount for the damage caused to the third party.

The Regional Transport Office (RTO) is the organisation of the Indian government responsible for maintaining a database of drivers and vehicles for various states of India. In addition, the RTO issues driving licences, organise a collection of vehicle excise duty and sells personalised registrations. Along with this, the RTO is also responsible for inspecting vehicle insurance and clearing the pollution test.